Read in Other Languages

Why One Oil Shock Caused 12 Different Inflations

Same Shock, Different Worlds: A Monetary-Regime View of Global Prices

In early 2026, almost every major economy saw its inflation rate tick up at the same time. The trigger was shared and singular: oil prices rising on Middle East tension. Energy is the one cost that feeds everything at once — transport, food, production — so when it moves, it moves the whole price level with it. Economists call this cost-push inflation.

But here is the puzzle. If the shock was the same everywhere, why does the long-run damage look so different from one country to the next? Over fifteen years, prices in the United Kingdom rose more than fifty-eight percent, while in Japan they barely moved at all. The answer is that an energy shock lands on top of each economy's own demand structure and its own central bank — and those differ enormously.

Cumulative Inflation by Country (grouped by monetary regime)

| Country | Latest Annual % | 10-Year | 15-Year |

|---|---|---|---|

| Netherlands (EUR) | 2.8 | 39.43% | 49.08% |

| Euro Area (EUR) | 3.0 | 33.36% | 39.46% |

| Germany (EUR) | 2.9 | 29.44% | 36.70% |

| Spain (EUR) | 3.2 | 30.77% | 34.85% |

| Italy (EUR) | 2.7 | 19.57% | 29.64% |

| France (EUR) | 2.2 | 18.10% | 26.55% |

| United Kingdom (GBP) | 2.8 | 41.43% | 58.20% |

| United States (USD) | 3.8 | 38.60% | 48.05% |

| Canada (CAD) | 2.8 | 29.01% | 38.00% |

| South Korea (KRW) | 2.6 | 17.06% | 31.79% |

| China (CNY) | 1.2 | 4.77% | 26.66% |

| Japan (JPY) | 1.4 | -1.30% | 1.90% |

Sources: officialdata.org (CPI cumulative, per country); Trading Economics (latest annual rates, April 2026). 2026 values provisional.

1. Where Inflation Ran Hottest: Demand

The countries with the largest fifteen-year price increases — the UK (+58%), the Netherlands (+49%) and the United States (+48%) — share a common engine: strong demand. Robust consumer spending, combined with the post-pandemic surge of 2021–2023, locked in a permanently higher price level. When people have money and want to spend it faster than the economy can produce, prices rise. This is classic demand-pull inflation, and the energy shock simply added fuel to a fire that was already burning.

2. The Opposite Problem: Asia

Now look at the other end. China's prices rose nearly twenty-seven percent over fifteen years, but almost all of that is old — the last decade added under five percent. Japan sat in outright deflation, with prices actually falling over the last ten years. This is not price stability; it is the symptom of a deeper problem: missing domestic demand. Two of the world's largest economies are stalling, and for them a dose of imported inflation is almost welcome.

3. The Currency Channel

In Korea and Japan, the recent rise was not really about demand at all. A weak local currency made imported energy more expensive in local terms — so their inflation was driven by the exchange rate. The same barrel of oil costs more when your currency is weak, regardless of how hot or cold your domestic economy is.

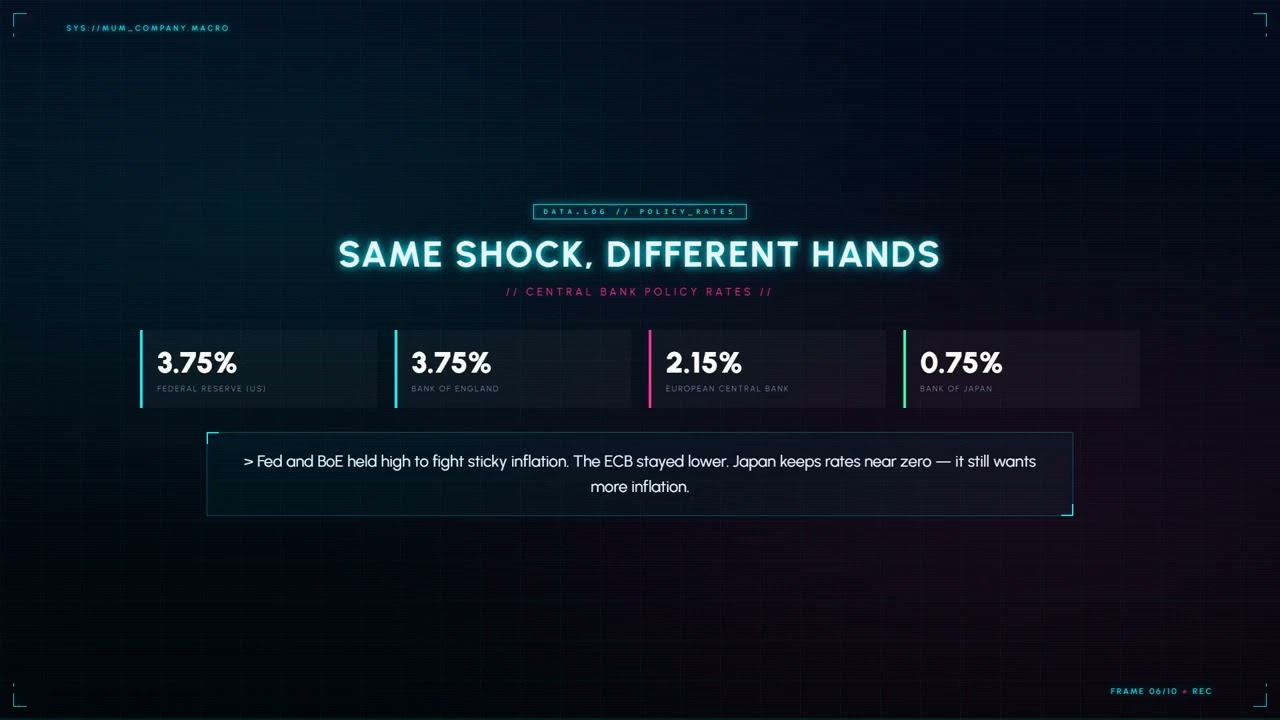

4. Same Shock, Different Central Banks

The final layer is policy. The same shock landed differently depending on each central bank's stance:

- U.S. Federal Reserve & Bank of England (~3.75%): held rates high to fight sticky service inflation.

- European Central Bank (~2.15%): stayed lower, because euro-area demand is softer.

- Bank of Japan (~0.75%): kept rates near zero, because Japan still wants more inflation.

5. The Euro Trap and the ECB's Dilemma

The hardest case is the euro. Inside the single currency, every country shares one interest rate — yet the Netherlands ran nearly fifty percent inflation over fifteen years while France stayed near twenty-six. Same central bank, same rate, opposite outcomes.

A shared currency without a shared budget is a cart pulled by two horses running in opposite directions. There is no single rate that fits both — one size fits no one.

That leaves the ECB in a trap with no good move. If it raises rates to cool overheating economies like the Netherlands and Germany, it crushes high-debt members like Italy, risking a debt crisis. If it cuts rates to help France and Italy, it pours fuel on Dutch and German inflation.

The Real Lesson

“Global inflation” is really two layers. On the surface sits a shared energy shock — the war premium on oil. Underneath sits each country's very different demand. Strong economies turn the shock into lasting price increases; weak ones absorb it and stall. And where a currency is shared but budgets are not, central banks are forced to optimise for an average that fits none of their members.

For a reader in Canada, the practical takeaway is moderate: roughly thirty-eight percent cumulative inflation over fifteen years — real erosion of purchasing power, but middle-of-the-pack rather than a crisis. The most important investment, as always, is understanding where your money's value actually went.

Data sources: officialdata.org (CPI-based cumulative inflation, per country); Trading Economics (latest annual and policy rates, April 2026). 2026 figures provisional. Country-level driver attributions are interpretive.